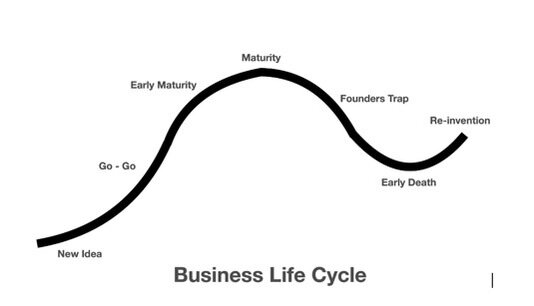

Business Life Cycle

Like people, companies go through various stages. This is called the business life cycle. From an exciting new idea for a product or service, companies seek security in their market. Early in this cycle the new idea captures all the activities of the company. The allure of garnering millions of dollars of revenue is the dream of the founders. Richard Branson, the British entrepreneur and successful founder of the Virgin Group once joked that it’s rather easy to become a millionaire. You simply start as a billionaire, then go into the airline business. Although this is a humorous anecdote, it does depict the experience of a multitude of companies. These companies don’t successfully move from the new idea phase of the business life cycle through the Go-Go stage (company is experiencing rapid growth), taking advantage of their first mover position. There are many examples of first movers that did not succeed in their market. For example, before Facebook, there was a social media company called Friendster. Before Google, there was Netscape. These companies couldn’t survive the Go-Go phase of their business life cycle.

The Go-Go phase of the company is where the founders vision dominates the daily work. Systems are put in place, both in anticipation of what is needed and as a reaction to developing problems or needs. “You don’t know what you don’t know” is an ample description of the environment and culture of the company. Success in the market leads to the need to manage growth. This can be a drain on both financial and human resources. The speed at which a given product, technology or market can evolve will have a significant impact on the Go-Go stage of your company.

The Go-Go stage is the ‘melting pot’ phase of your company. In addition to the costs associated with blazing a new trail, key personnel are added. Each of these key staff members have various talents and experiences. They also come from different cultures to a place where none exists. “This is how we did this at ____________,” (former company) becomes the norm unless management sets clear examples and expectations. It can be as simple as getting to work in the morning or finding a parking spot. If management arrives at 9:00 AM every morning, they set the tone for the business. “This is when work starts”. Long lunches, meetings without agendas, action plans without follow through set the tone for the employees, creating the discipline or lack of discipline in the operation of the business.

To illustrate; who is the manager you would rather work for, or emulate? Manager “B”, who arrives between 9:00 and 9:30 every morning. Walks into his office, closes the door until 12:00 PM when he departs for a one-and-a-half-hour lunch. Upon his return, he accepts meetings by appointment only. Once a month, he conducts a staff meeting with-no agenda or follow through from previous meetings. These meetings consist of the staff hearing a dissertation on the business. Input is not welcomed.

Manager “O” arrives promptly at 6:00 AM every morning. She uses the first hour to clear her desk and attend to projects that need her immediate attention. She expects the staff to arrive between 7:00 and 7:30 where she welcomes them with an “open door” policy. She spends the first hour of their day checking in with them (note: Deming called this management by walking around) on their progress, issues and needs for the day. If decisions or guidance are needed, “O” provides it on the spot. When staff meetings are held, an agenda is organized with input from the staff. Follow up from previous meetings are commonly done during these sessions. “O” is typically the first to arrive and the last to leave. She doesn’t need a reserved parking spot. Her philosophy is to get to work on time and there is no need to compete for parking.

Who would you rather work for? What qualities does the “best manager” have that would guide you on your management journey?

People fall into three categories: starters, maintainers or finishers. As a manager, it is important for you to know the characteristics of your staff. The Go-Go phase normally accumulates lots of starters. There are new opportunities within the business to tackle.

As you make progress, you move to the next phase called “early maturity”. This is where the company requires more “maintainers” as well as “finishers”. Leaders evolve during this phase. This is the phase where the company grows up. The focus is no longer on discovering how to conduct the business. To your customers, you have an identity. Expectations and the personality of the company drive the reputation in your industry. Because early maturity is a growth phase, this is where staff are added. Competitive pay and benefits become a focal point for staff. Discipline in people and process is the focus for management. Disciplined financial management results in the implementation of a budgeting process to align the resources of the company with the revenue plan.

Mature companies are responsive to their stakeholders: customers, employees and shareholders. This is demonstrated by applying lean management principals where strong financial management is utilized without sacrificing the building blocks of the company. Management has to change during each phase of the business life cycle and failure to adapt and change will inhibit growth. Mature companies provide growth opportunities and seek talent that will propel the company’s growth and future. The founders typically recognize that an infusion of resources with “new skills” are necessary for challenging the “status quo” of the business.

Founders Trap occurs when the founder(s) cannot separate themselves from all aspects of the business and effectively delegate. During the start-up and the go-go phase of the company the founders are forced to wear lots of hats and “be experts” on all operational needs of the business. Founders often confuse wearing these hats to being better at managing these tasks than anyone who may follow them.

Organizations needs to clearly communicate responsibilities and delegate decisions that further its strategies. Distributing the founder’s responsibilities is essential to building a more valuable company. The founder’s job is to build a strong management team to address issues and distribute accountability. A quality management team is required to avoid “death” of the organization. The founder must ensure the right people are in place (the right seat on the bus) to move the company forward.

Without a strong management team where decisions, responsibility and authority are distributed the organizations pace of change will be limited by the ability of the founder to intervene in all aspects of the business.

Contact us to discuss an assessment of your business life cycle.

Why Be in Business?

If we only would have had more time! If we only would have had more money to start! If we only ……(fill in the blank). Most new businesses fail. Most mature businesses fail or give way to others that make continued progress over time and react to the changing environment. People always change. Customer needs and perceptions always change. The one thing any business must ask themselves is ‘what problem is my product or service solving’? How does my solution bring value to the consumer? What are people willing to pay?

We often fall in love with our own ideas. We typically surround ourselves with others, ‘yes men’, who encourage us by agreeing with our own ideas regardless of how ridiculous they sound to them.

For example, I was introduced to a couple of guys who wanted to pitch their business idea to me. They were hoping for some input. I sat patiently while they described their idea for a consulting business. I kept thinking, what is the product? What is the service? What are they selling? When they finally finished, they looked at me with big eyes and said “what do you think”? My mother’s words kept resonating in my head…be nice, be nice. Seconds felt like minutes as I tried to think of what to say. I decided to ask a few qualifying questions. Who is the target customer? What is the source of your data? Describe the delivery process. What materials will your customers receive? They had no answers, but they had one additional and immediate question: “what do you think we can charge”? After a short pause where I collected by thoughts, I told them I wouldn’t pay anything. I explained to them that they hadn’t demonstrated anything in their proposed company that offered any value. “Look guys”, I said, “to be honest with you, if you came to pitch me on your company, I would be looking at my watch, trying to figure out how quickly I could get you out of my office. You need to pass the Mom Test”.

The Mom Test

The “Mom Test” by John Mullins is a book that provides a simple lesson on vetting your business ideas. Don’t ask your Mom! Don’t ask your friends! They will all lie to you. They don’t want to hurt your feelings. If you want candid input on your business ideas, pass the Mom Test. Don’t ask leading questions. Don’t seek input from “yes men”.

Note: “Yes Men” can always be counted on to agree with the boss. No matter what is said or asked, they agree. It doesn’t matter how stupid or insane the idea might be. If a boss told a “yes man” to pee in a corner, they would. They would never question if they were in the right corner. Yes Men “aim” to please.

Discuss your product or service in general terms, instead of your specific idea. Seek specifics in your client’s past experiences instead of generic opinions about the future. These guys failed the Mom Test because they had a solution seeking a problem.

Rule of thumb: Don’t confuse good ideas with blind ambition or as my Dad once said, “don’t be fat, dumb and happy about your own ideas”. Before launching into business ask yourself the “what” questions.

• “What is the problem you’re attempting to solve?”

• “What is the opportunity you’re trying to take advantage of?” Sometimes the company doesn’t actually have a problem; it just wants to take advantage of an opportunity.

• “What is the information/data you need to record and store?” Businesses live on information, so they have to understand the data they need. Asking “What information will you need in order to make decisions in your daily operations?”

Your Market

Marketers are in constant search of “trying to influence the influencers”. From celebrity endorsements to infomercials, marketing professionals flood us with “new, improved or never seen before” products.

In his book, Crossing The Chasm, Geoffrey Moore applied the principal of high tech marketing to the five segments of customers: innovators, early adaptors, early majority, late majority and laggards. Called the Law of Diffusion of Innovations, it states that the first 2.5% of the population are the innovators and the next 13.5% are the early adapters. Innovators and early adopters need to be first. These are the people that wait in line for the new phone the day before it comes on the market. For them it’s a status symbol and they will accept defects or product flaws in order to be first. They accept risk and heavily rely on their intuition when making purchasing decisions.

Law of Diffusion of Innovation

Innovators expect to pay a high price for new products. Early adopters expect to pay a premium. This has less to do with how great the new product may be and more to do with their own sense of who they are. Success with early adopters can launch a company or solidify a company in the marketplace.

Consider the scenario where you introduce a new product but after six months it only represents 2% of your revenue stream. Your marketing department may want to pour more money into marketing campaigns trying to convince management that the product is showing signs of success. The ‘brutal fact’ is that you are failing. Your market penetration only captures the innovator segment of the market. You haven’t shown any signs of moving into the revenue generating segments of the market. It’s time to regroup and examine the problem.

The early majority is 34% of any market. Unless you can secure this segment, your company will lack security and never reach the Go-Go segment of your business life cycle. (Note: See Business Life Cycle)

Capturing the early majority means you have something of value, something to sell. Mass market success or acceptance has occurred.

Entrepreneurs dream of mass-market success, but it is hard to achieve. Of the 27,000,000 businesses registered in the U.S., fewer than 2,000 ever realize mass-market success, capturing the early majority and the late majority (which also makes up 34% of the market).

Note: Don’t worry about the Laggards. They are still using flip phones.

Mature Companies

One of the shortest segments of the business life cycle is the maturity phase. Companies can have a false sense of security during this phase. Operations are intact and business process is mature. It is a wash – rinse and repeat time for the business. The acquired reputation of the company drives customer attitudes towards it’s products and service.

For example, look at the automobile industry. This is a mature industry. Where cars once dominated, consumer preferences shifted to SUVs and pickup trucks. Ford has dominated the truck business for over 30 years. GM, Ford, Toyota, Daimler-Benz, etc. continue to flood the market with a wide variety of vehicles, but all of these companies lack something consumers look for: innovation for the future. The industry has operated on cruise control.

Enter Tesla. Is it the attraction of the all-electric vehicle, cost, innovation or elimination of barriers to entry that have propelled Tesla? Has Tesla done anything that GM, Ford or any other automobile manufacturer couldn’t do?

The maturity phase of the company means that the operating principals change. A conservative attitude prevails and management is adverse to taking risks. Even as competitive threats emerge, the founders refuse to acknowledge these threats adopting an attitude of what worked in the early stage of the company. Customers and consumers might change, these companies do not.

This is referred to as the Founders Trap, which can lead to early death. The railroad business didn’t understand they were in the transportation business. This is a well-known axiom. This ultimately led to the death of their business, which fell into the founders trap. A more modern version of this is the story of Apple.

Steve Wozniak and Steve Jobs were the original founders of Apple. Wozniak engineered the Apple I and Apple II computers to be simple enough to allow people to harness this new technology. In the first year of business, the new company sold $1 million worth of computers. By year two, they had sold $10 million worth of computers. They were in Go-Go land. In the third year, they sold $100 million. Apple continued to make progress and became a “mature” billion-dollar company, and that’s when the trouble began. They lost their mojo. Their innovation was gone, and the market moved decisively to IBM and the PC fueled by Bill Gates and Microsoft. Wozniak and Jobs continued to do the same thing; create the next computer. Doing the same thing, expecting a different result, is a symptom of the founder’s trap and leads to early death.

Jobs was fired by his own company. Apple continued to struggle and eventually brought Jobs back. It was an act of desperation. The best lessons are often the result of failure. Upon his return, Jobs knew that Apple had to “think different” to be different in a competitive world. “Think Different” became the mantra (WHY) for Apple. The company reinvented itself and has developed a culture where reinventing itself is expected. What was once a computer company, is now a __________ . (Note: fill in the blank: phone, digital music, hardware software, streaming, etc.)

Maturity does not automatically lead to long-term success.

Take away points:

1. Maturity in your market can give you a false sense of security.

2. You are never to big to fail.

3. Reinventing your company to create a culture designed to compete.

4. Avoid the Founders Trap: maintain an innovative culture by reinventing yourself.

Contact us to discuss an assessment of your business life cycle.